![]()

EU taxonomy: where does the German industry stand?

DAX40: no solutions for climate change (yet)?

An analysis by Maresa Bachmann, Teresa Stetter and Hendrik Leue.

From January 1st, 2023, the taxonomy reporting of the largest companies on economic activities will take place. But as early as 2022, capital market-oriented companies that were already subject to non-financial reporting obligations were obliged to declare their taxonomy eligibility. This includes the disclosure of all economic activities, broken down into turnover, capital expenditures and operating expenditures, that make a significant contribution to climate protection or adaptation to climate change.

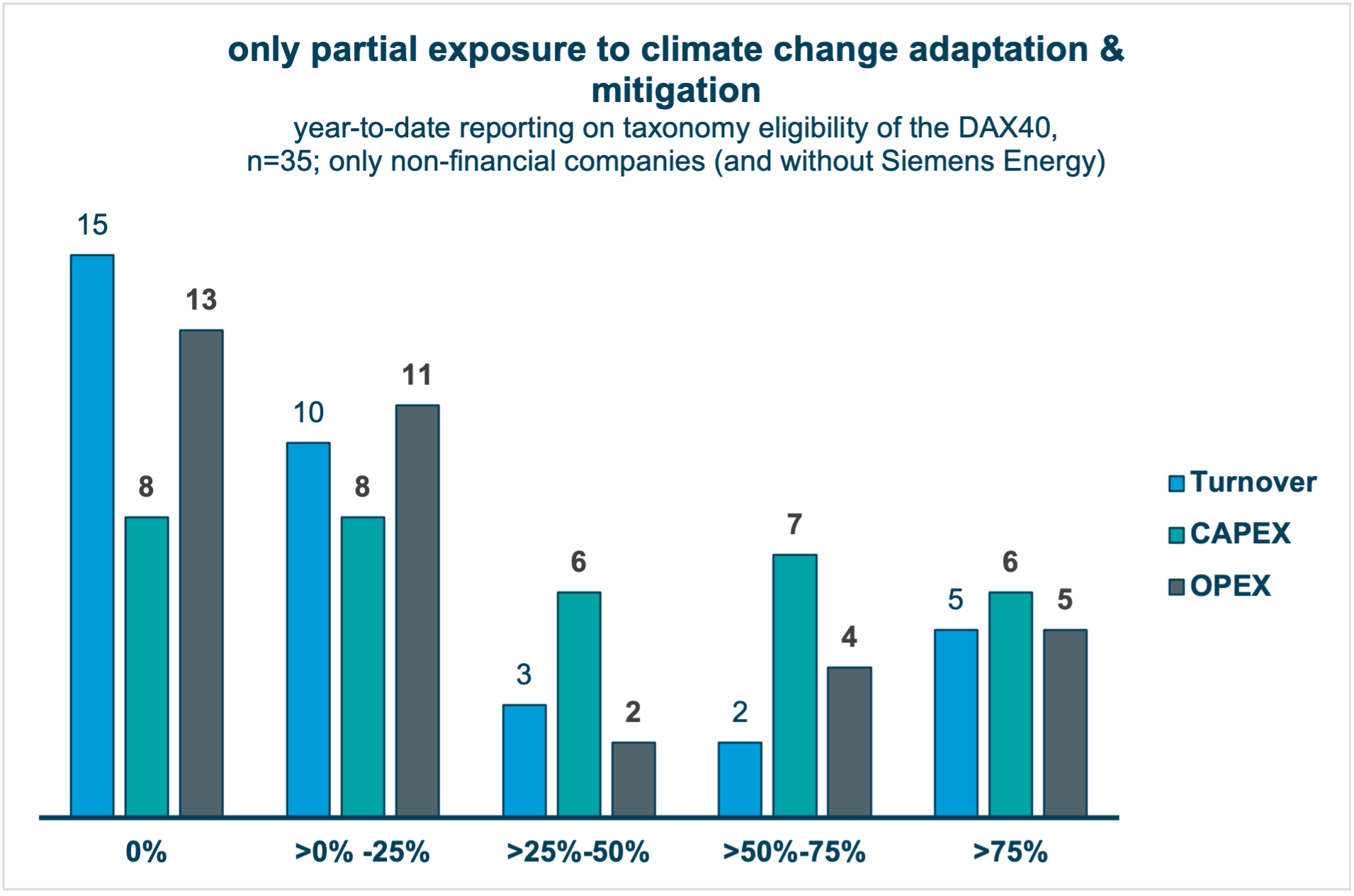

An evaluation by fors.earth showed very heterogeneous results with regard to the largest listed companies in the DAX.

Almost half of the evaluated (non-financial) companies report 0 % turnover and also operating expenses (OpEx). Only ten companies report more than a quarter of turnover as generally taxonomy-eligible; this number is even lower for operating expenses. A stronger normal distribution results for companies' capital expenditure (CapEx). Only a minority does not report any taxonomy-eligible expenditures.

With regard to the turnover eligible for taxonomy of DAX companies, a certain skepticism is warranted that climate change is already a current business opportunity for German industry. However, the higher level of reported taxonomy-eligible investments at least suggests that future business areas will be developed with a view to climate change or existing business areas will be adapted with regard to climate compatibility (e. g. with the help of investments in renewable energies).

Outlook – Opportunities beyond climate

In order to put these results in context, it is important to note that so far only two of the six environmental objectives of the EU taxonomy have been defined in a delegated act. According to official planning, another delegated act for the remaining four environmental objectives will come into force in December 2022. So far there is only a draft of the Platform for Sustainable Finance for the criteria.

It will therefore only be possible to analyze the extent to which companies contribute to the all environmental objectives for 2023. The following goals still need to be defined:

- Sustainable use and protection of water resources

- Transition to a circular economy

- Avoidance of pollution

- Protection of ecosystems and biodiversity

In some cases, other business areas of companies from the DAX40 could also be included in these environmental objectives. For example, according to the current draft, the trade and manufacture of textiles (possibly Zalando, Adidas, Puma) would be taxonomy-eligible, as would certain areas of the chemical industry (possibly BASF, Beiersdorf, Henkel).

Furthermore, there is a prospect of expanding the taxonomy to include social objetives, although the criteria for this might not be limited to the business areas. The overall objectives proposed by the platform so far

-

"good work",

-

"adequate living conditions and well-being of consumers" and

-

"inclusive and sustainable social development"

can be applied both at the level of products and services as well as to companies' own operational effects. This opens up other areas of industry for taxonomy-eligible economic activities – especially companies with offers in the area of basic human needs (housing, health) should be excited about this extension of the taxonomy.

Case Studies: Reality of Alignment Testing

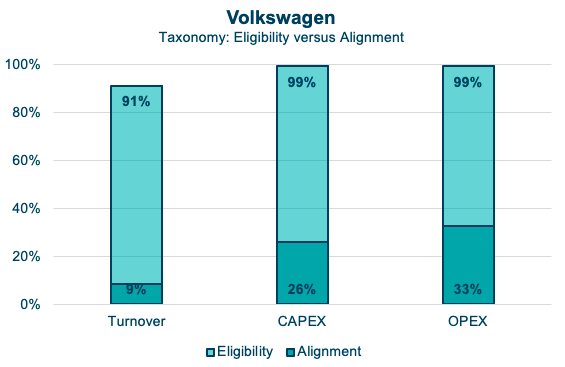

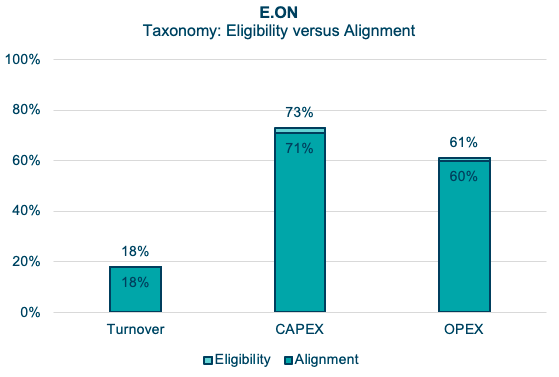

Only two DAX companies have already voluntarily reported on the proportion of taxonomy-aligned economic activities in 2022: the utility company E.ON and the automotive group Volkswagen, two companies with a particularly high proportion of taxonomy eligibility.

Source: VW Sustainability Report 2021

Both companies report in detail which assumptions and derivations the calculations for taxonomy capability and compliance are based on, but use different approaches.

Volkswagen generally generously identifies economic activities as eligible to the taxonomy, especially with regard to taxonomy number 3.3. "Production of low-CO₂ transport technologies".

According to this, the proportion of aligned activities is reduced as a result of the application of the criteria for the substantial contribution to climate protection, since the proportion of climate-friendly mobility solutions is currently still low. The DNSH criteria and minimum safeguards criteria only “burden” the quotas minimally.

The picture is different for the utility and grid company E.ON.

Source: Annual Report 2021

In contrast to Volkswagen, E.ON can refer to significantly more clearly defined taxonomy-eligible activities in its core business. A total of nineteen categories – such as 4.9 “Transmission and Distribution of Electricity” – are relevant for E.ON. In contrast to Volkswagen, no further criteria for the substantial contribution are defined in many business areas, such as electricity generation from wind and solar power. In other words: All wind energy activities count as a substantial contribution.

The DNSH and minimum protection criteria are treated very briefly in E.ON's first taxonomy report. Reference is made to already established sustainability-related processes, such as environmental assessments, to discuss compliance with the criteria.

Conclusion

The EU taxonomy reporting will keep companies busy in the next few years and the introduction of the CSRD will extend the application of the taxonomy obligation to up to 15,000 companies in Germany.

The content requirements are also becoming stricter. Not only will new environmental objectives be added and possibly also supplemented by social ones, in the short term there will also be greater challenges from the obligation to report full taxonomy conformity and from the stricter application of formal requirements such as the use of special templates.

Companies should therefore position themselves well in three areas in particular:

1) Know-how and knowledge transfer

Employees must gain an understanding of the content-related test criteria and formal requirements. This often goes beyond those responsible for sustainability, since the operational departments are often essential for determining taxonomy-relevant data

2) Establish processes and practice procedures

Internal processes must be designed in such a way that data collection and aggregation can be carried out efficiently, but above all in a comprehensible and high-quality manner. Solid processes can also help to exploit existing taxonomy potential.

3) Make taxonomy strategically usable

Finally, companies should think about how they can turn the obligation to report into a strategic advantage. After all, the taxonomy is a tool to increase the sustainability impact of the financial and real economy and can help companies to document their own ecological impact and to control it in the long term.

fors.earth is happy to support you with your taxonomy reporting.