Behind the scenes of EFRAG's LSME community

Our Senior Advisor on Sustainable Finance Hendrik Leue has been selected to help shape EFRAG's CSRD reporting standards for listed SMEs.

Since the beginning of January 2023, Hendrik Leue – Senior Advisor for Sustainable Finance – has been working in the so-called LSME Community of EFRAG.

Their task includes the development of future reporting standards according to CSRD for small and medium-sized companies that are listed on stock exchanges. This includes around 1,100 companies in Europe and 100 in Germany.

In addition, under the scope of these standards, there are the so-called "small and non-complex institutions" from the financial sector. In Germany, this refers primarily to the local savings and cooperative banking sector with over 1,000 institutions. Furthermore, so-called captive insurance and reinsurance companies are subject to these standards.

Hendrik, what made you decide to take part?

Working with companies and investors on their sustainability strategy and implementation is of course exciting enough. And currently more and more companies are approaching us which so far have made relatively little effort to integrate sustainability into business processes. For many, the switch has now been flipped with the forthcoming regulation.

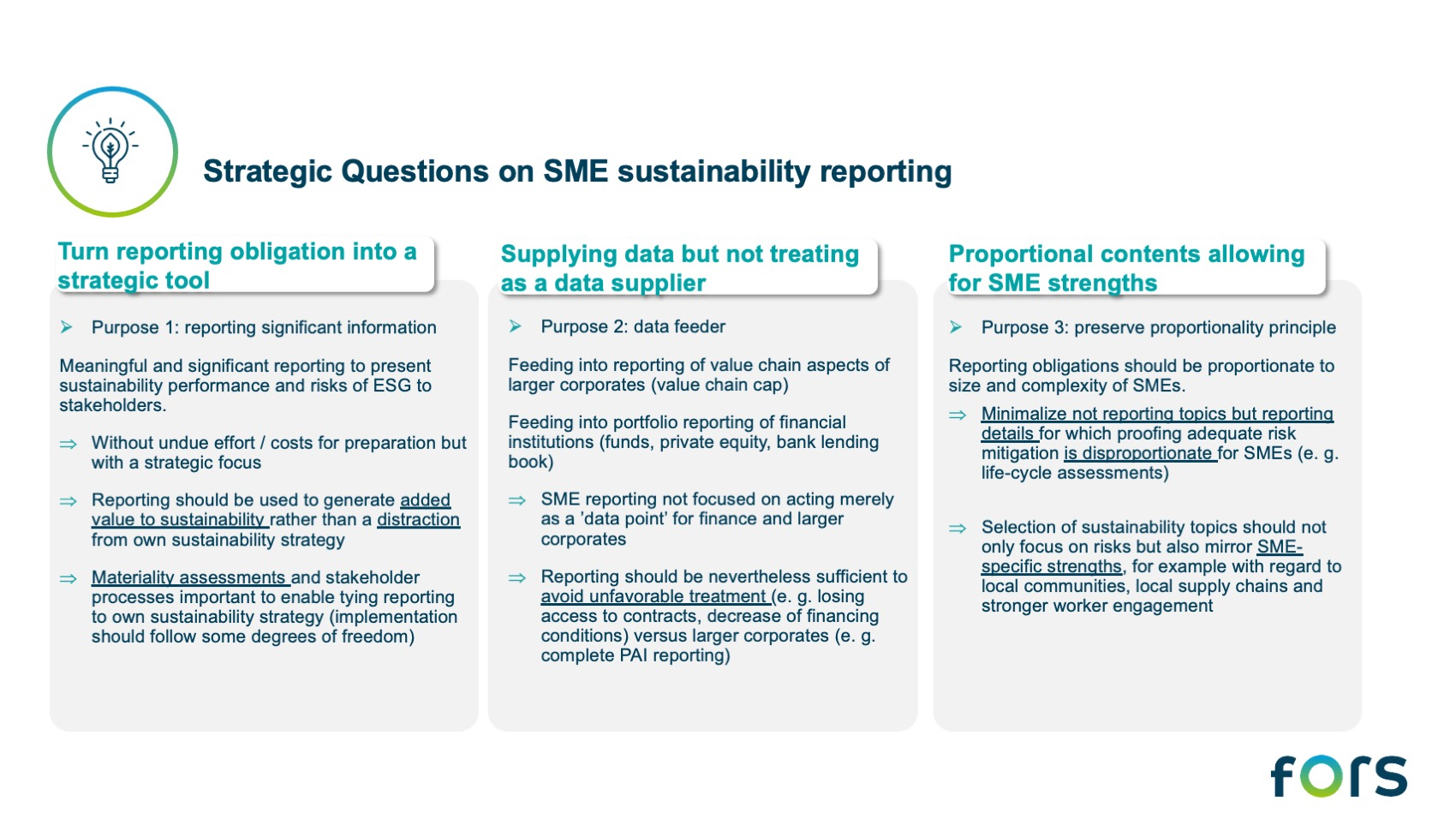

Although it is primarily about reporting obligations, these serve as an incentive to become more active in many other areas. As consultants, we should try to support companies in turning this task from a "chore" into a strategic advantage.

Therefore, in the process at EFRAG, I would also like to emphasize the aspect that smaller companies can definitely derive a strategic advantage from the reporting obligation and not only serve as a data supplier for large corporations and financial investors.

How transparent is the standard setting process? What is discussed in public meetings? How can interested parties participate in them and follow the results?

There was a public call for attendance at the end of 2022 so that experts from the field could work on the details together with the EFRAG secretariat. The working group consists of people with diverse backgrounds from all areas and countries. A distinction is made between the group of "users" of sustainability data – such as larger companies and financial market participants – and the group of so-called "preparers", i. e. the SMEs who actually have to compile the reports. With my work at fors.earth, I belong arguably to both groups: I personally work a lot for financial market companies, which would be users. But at fors.earth we also have many customers in the area of small and medium-sized companies, which are prospective preparers.

The hearings are non-public within the group. However, during the last 40 minutes of the hearings, EFRAG opens the session to the public – most recently on 27 January. Interested parties can then listen to a summary of the closed session discussions and participate in discussing the issues with other interested stakeholders. So far, this option has met with great interest and demand, especially among SMEs. Interested parties can register here to attend a public session.

What challenges do you currently see in designing the ESRS?

The design of the ESRS for smaller companies is subject to some constraints. For example, the CSRD stipulates that the reporting obligations should also be lower in proportion to the size and complexity of the company. That proportionality approach seems evident. Those who have fewer resources should also have fewer obligations. From a sustainability risk point of view, this is usually completely fine, because small and medium-sized companies usually have a significantly smaller direct footprint and, due to less complex value chains, often fewer indirect risks – such as human rights in the supply chain.

However, the reporting obligations must serve not only the company’s own portray of sustainability, but also fulfil the requirements of other parties. One of the general purposes of the CSRD is to provide investors with sufficient sustainability information and thus also to promote more sustainable business models and processes. Financial institutions must publish standardized key figures, the so-called PAIs (Principle Adverse Impacts) about their portfolios and hence require also smaller companies to provide such data. And smaller companies should not be excluded from financing just because they publish less sustainability data.

The other purpose, according to the CSRD, is that the reporting obligations for SMEs are also decisive for the extent to which large companies report with regard to their value chain. In other words: if SMEs, for example, do not have to report anything about their climate risks, this also reduces the reporting obligations for large corporations on their upstream or downstream climate impacts.

Therefore, there is a certain conflict of goals between expanding the reporting obligations in the interests of the users (financial market, corporations) and focusing on the interests of the SMEs and the proportionality approach.

What will become important for SMEs?

In my view, the conflict of goals mentioned will not only be resolved through a clever design of the reporting obligations. It would be a pity if the greater degree of sustainability reporting in larger companies meant that corporations secured even more market share than smaller companies.

I therefore advocate that small and medium-sized companies also go through a sustainability process that is as robust as possible, which can be used strategically and profitably, instead of being perceived as just drawing resources. For me, this includes a strong position of the materiality analysis. In a CSRD-compliant materiality analysis, fewer topics will tend to be classified as material for SMEs, since the factors "scale" and "scope" should objectively be lower when viewed from the inside than in comparable large corporations.

In the process of the materiality analysis, specific strengths of smaller companies can better come into play – for example, the involvement of external stakeholders. Small companies know their employees better, tend to maintain regional supply relationships and sales channels. They are often deeply rooted in local communities. It is important to promote and highlight these advantages. If this succeeds, it will also become increasingly worthwhile for smaller companies to consider and promote sustainability as a strategic aspect of their own business processes.

When these factors are taken into account, SMEs can act as confident actors and avoid reporting obligations relegating them to being mere “data providers” to third parties.

In addition, however, everything should be done to support SMEs in the processes. The EFRAG panel has already addressed the extent to which prepared templates and reporting tools can be made available. In addition, I expect that the processes in matters of materiality analysis will experience a clear professionalization in the next few years. This also reduces costs for SMEs, which will only actually be subject to CSRD reporting from 2028.

Are there any topics that you think should be discussed more?

Over a thousand smaller financial institutions from Germany, mostly savings banks and cooperative banks, are among the companies covered by the reporting requirements for SMEs. Across Europe there are even more than two thousand institutes, together more than the real economy companies that are listed on stock exchanges.

To me the fact that these institutes will also have to report more on sustainability aspects in the future seems to be underrepresented in the debate at the moment. Especially in Germany's fragmented banking market, this could still be decisive as to whether local institutions can subsist beside the big ones. Yet savings and cooperative banks in particular, with their strong local focus, actually have the opportunity to credibly set themselves apart from the large institutions in terms of sustainability. To do this, however, sustainability would have to be recognized as a strategic issue. The old slogan "we have always been sustainable", in the sense of being on the market for often hundreds of years, is no longer sufficient. Perhaps the reporting obligations can herald a rethink here as well.

What is the next milestone?

By mid-2024, delegated acts are to be enacted to lay down the reporting obligations. In fact, due to the interweaving with the reporting obligations of large companies, these legal acts may possibly come about before that. I think it is relatively likely that the elaboration will come as early as the first half of 2023 in order to be able to be implemented together with the ESRS for large companies.

What do you wish for from EFRAG?

The openness to being able to use the reporting obligations as a gateway for companies to deal more intensively with the topic of sustainability in operational terms. To this end, the reporting obligations should also allow and promote strategic elements. In this way, sustainability reporting can be transformed from a chore into strategic fun.